Direct lending is defined as a financing arrangement where a borrower receives funds directly from the capital source, with no intermediary involved in the transaction. Indirect lending, by contrast, routes the loan through a broker, dealer, or other intermediary who connects borrowers with lenders. The choice between direct lending vs indirect lending shapes your total cost, approval timeline, and negotiating power. For individuals and businesses across the APAC region, where cross-border deals and complex credit profiles are common, understanding this distinction is not academic. It is a decision with real dollar consequences.

What is the difference between direct and indirect lending?

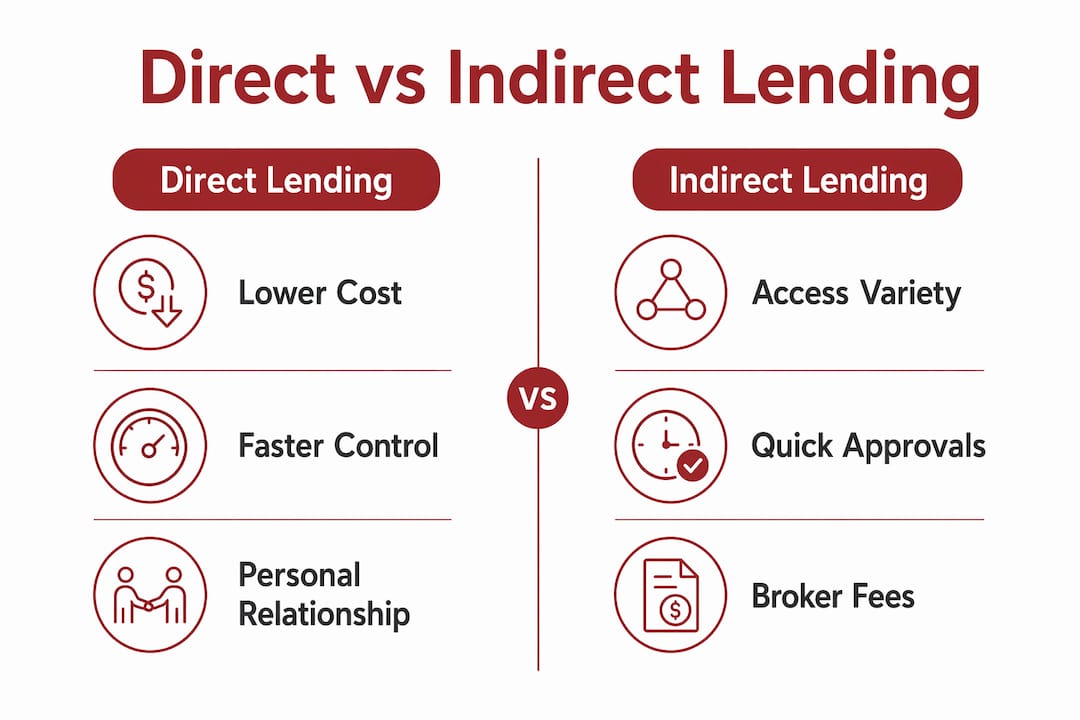

Direct lending places the borrower in a one-on-one relationship with the lender. The lender underwrites, funds, and services the loan entirely in-house. There is no middleman setting terms or collecting a fee between the two parties. This structure gives the borrower a direct line of communication and, critically, a single decision-maker to negotiate with.

Indirect lending introduces a broker or dealer into that relationship. The intermediary shops the borrower’s profile across multiple lenders, collects competing offers, and presents options. The convenience is real. The cost is also real. Broker fees typically range from 1% to 5% of the loan amount, either charged directly or embedded in the interest rate. On a $250,000 loan, a 3% broker fee adds $7,500 to the total cost of borrowing.

Regulatory bodies across APAC, including the Monetary Authority of Singapore (MAS) and the Australian Prudential Regulation Authority (APRA), govern both lending structures. Their disclosure requirements affect how fees and terms must be presented to borrowers. Understanding which rules apply to your transaction is a foundational step before choosing a lending channel.

How does direct lending work, and what are its benefits?

Direct lenders conduct their own underwriting, hold the loan on their balance sheet, and manage the borrower relationship from origination through repayment. This end-to-end control is the source of most direct lending benefits.

Asset-based underwriting and faster approvals

Direct lending underwriting focuses on collateral value and liquidity rather than extensive income verification. This approach suits APAC businesses with strong asset bases but irregular income streams, such as property developers, logistics operators, or early-stage manufacturers. Documentation requirements are typically lighter than traditional bank financing.

Technology-enabled direct lenders now integrate real-time financial data from accounting systems directly into the credit assessment process. This integration expands access to financing for commercially viable businesses that fall outside conventional bank credit criteria. For a small business owner in Vietnam or Indonesia, this can mean the difference between securing growth capital and being turned away.

Direct loan closings for straightforward transactions typically take 1–3 business days. That speed matters when a business needs to move on a time-sensitive acquisition or supply chain opportunity.

Credit performance and risk management

Direct lending carries a cumulative loss rate of around 1.33% over five years. Leveraged loans carry a 3.1% loss rate, and high-yield bonds carry 4.2%. That gap reflects the structural discipline built into direct lending: proprietary due diligence, covenant protection, and ongoing borrower monitoring.

When a loan runs into trouble, direct lenders hold a structural advantage. Because a single lender holds the entire credit facility, workout amendments and forbearances can be completed in weeks rather than months. There are no intercreditor disputes, no syndicate votes, and no competing agendas. For a borrower facing temporary distress, that speed of resolution can preserve the business.

Key direct lending benefits for APAC borrowers include:

-

Faster credit decisions, often within 1–3 business days for simple cases

-

Lower total borrowing cost with no intermediary fees

-

Direct negotiation with the decision-maker on terms and covenants

-

Asset-based underwriting that suits non-traditional income profiles

-

Bilateral workout control if the loan needs restructuring

Pro Tip: If your transaction involves real property, equipment, or inventory as collateral, a direct lender’s asset-based underwriting model will typically produce a faster and cheaper outcome than routing through a broker.

What are the advantages and trade-offs of indirect lending?

Indirect lending earns its place in the market through one primary advantage: access. A broker with relationships across 20 to 60 lenders can present a borrower’s profile to multiple capital sources simultaneously. For borrowers with complex credit histories, non-standard income, or cross-border structures, that breadth of access can unlock financing that a single direct lender would decline.

Speed and convenience at a cost

Indirect lending approvals can arrive in minutes to hours. The broker handles the legwork of packaging the application and distributing it. For a borrower who lacks the time or expertise to approach multiple lenders individually, this is a genuine service. The trade-off is cost and transparency.

Broker compensation may come from the borrower as an upfront fee, from the lender as a yield spread premium, or from both. When the fee is embedded in the interest rate, borrowers often do not realize they are paying it. A yield spread premium of 1% on a $500,000 loan over five years adds far more than the nominal fee suggests once compounding is factored in.

Indirect lending also creates a communication barrier. The borrower negotiates with the broker, not the lender. If the lender has questions or conditions, they pass through the intermediary. This layer slows down complex negotiations and can distort information in both directions.

Scenarios where indirect lending makes sense:

-

Credit profiles that do not fit a single lender’s criteria

-

Borrowers who need multiple competing offers to negotiate from strength

-

Transactions where the broker’s lender relationships provide access to specialized capital

-

Situations where the borrower lacks the capacity to manage multiple lender relationships directly

Pro Tip: Always ask the broker to disclose their compensation in writing before signing any engagement letter. Request a breakdown of whether fees come from you, the lender, or both. This single step prevents most hidden-cost surprises in indirect lending.

How do direct and indirect lending compare on cost, speed, and control?

The core comparison between direct vs indirect lending comes down to four variables: cost, speed, control, and flexibility. Each lending type excels on different dimensions.

| Factor | Direct lending | Indirect lending |

|---|---|---|

| Approval speed | 1–3 business days for simple loans | Minutes to hours via broker |

| Total cost | Lower; no intermediary fees | Higher; broker fees add 1–5% of loan amount |

| Underwriting focus | Asset-based; collateral and liquidity | Varies by lender; broker packages the file |

| Borrower control | Direct negotiation with lender | Negotiation mediated through broker |

| Workout flexibility | Bilateral; fast resolution | Depends on lender; broker not involved post-funding |

| Access to options | Single lender’s criteria | Multiple lenders via broker network |

Direct lending’s structural advantages in workout and modification scenarios are particularly relevant for APAC businesses operating in volatile markets. A Singapore-based manufacturer with operations in Thailand or Malaysia faces currency, regulatory, and supply chain risks that can affect loan performance. Having a single lender who can move quickly on a covenant waiver or repayment restructure is a material risk management tool.

Technology is reshaping both models. Direct lenders now use real-time data feeds from accounting platforms like Xero and QuickBooks to underwrite loans faster and with greater accuracy. Indirect lending platforms aggregate lender offers through digital marketplaces, reducing the time brokers need to shop a deal. Both trends benefit APAC borrowers, but they do not eliminate the fundamental cost difference created by intermediary fees.

A common misconception is that indirect lending always produces better terms because brokers create competition among lenders. This is only true when the broker’s network is genuinely broad and the borrower’s profile is attractive to multiple lenders. For straightforward transactions with strong collateral, direct lending almost always produces a lower all-in cost.

How do you decide between direct and indirect lending?

Choosing between the two lending types requires an honest assessment of your credit profile, timeline, and cost tolerance. There is no universal answer, but there is a clear decision framework.

-

Assess your credit profile. If your financials are clean, your collateral is strong, and your income is verifiable, a direct lender will likely approve you faster and cheaper. If your profile is complex or non-standard, a broker’s access to multiple lenders adds real value.

-

Define your timeline. Direct lending closes in 1–3 business days for simple deals but may take longer for complex structures. Indirect lending can produce offers in hours but may slow down during negotiation.

-

Calculate total cost. Add broker fees, yield spread premiums, and origination points to the interest rate before comparing offers. A lower stated rate with a 3% broker fee often costs more than a higher stated rate with no fee.

-

Evaluate lender transparency. Direct lenders disclose their own terms. With indirect lending, clear fee disclosure from the broker is non-negotiable. If a broker resists disclosing compensation, treat that as a warning sign.

-

Consider post-funding needs. If you anticipate needing covenant modifications or restructuring support, direct lending’s bilateral control is a significant advantage. Legal counsel familiar with loan restructuring processes can help you assess this risk before you sign.

For small business owners in APAC, the decision often hinges on speed versus cost. A retail operator in the Philippines needing working capital in 48 hours may accept a broker’s fee to access funds quickly. A property developer in Singapore with a clear asset base and a 10-day window will almost always benefit from going direct.

Pro Tip: For any loan above $500,000 or any cross-border financing structure, engage corporate finance legal counsel before committing to a lender or broker. The cost of legal review is small relative to the cost of a poorly structured loan.

Key Takeaways

Direct lending consistently delivers lower total cost and stronger borrower control, while indirect lending provides broader access and convenience at a measurable price premium.

| Point | Details |

|---|---|

| Cost difference is concrete | Broker fees of 1–5% add thousands of dollars to total borrowing costs versus direct lending. |

| Direct lending closes faster for simple deals | Straightforward direct loans close in 1–3 business days; indirect approvals are faster but costlier. |

| Loss rates favor direct lending | Direct lending’s 1.33% cumulative loss rate outperforms leveraged loans at 3.1% and high-yield bonds at 4.2%. |

| Indirect lending suits complex profiles | Brokers with 20–60 lender relationships provide access that a single direct lender cannot match. |

| Workout control matters | Direct lenders resolve distressed loans in weeks; syndicated or brokered structures take longer and involve more parties. |

What I’ve learned from watching APAC borrowers choose the wrong channel

The most expensive mistake I see is borrowers defaulting to indirect lending because it feels easier. A broker handles the paperwork, presents options, and creates the impression of a competitive process. But when I look at the total cost of those deals, the broker’s fee often consumes the rate advantage the borrower thought they were getting.

The second mistake is the opposite: borrowers with genuinely complex credit profiles approaching a single direct lender and getting declined, then losing weeks before pivoting to a broker. Knowing your own credit profile before you approach any lender saves time and preserves negotiating leverage.

What I find most encouraging in 2026 is how technology has shifted power toward borrowers. Real-time data integration means direct lenders can underwrite faster and with less documentation. Digital broker platforms mean indirect lending is more transparent than it was five years ago. APAC borrowers who take the time to understand both channels, and who get proper legal and financial advice before committing, consistently get better outcomes than those who move on instinct or urgency alone.

The regulatory environment in APAC is also tightening. MAS and APRA have both increased disclosure requirements for intermediaries. That is good for borrowers, but it also means the compliance burden on lenders and brokers is rising. Choosing a lender or broker who takes compliance seriously is not just an ethical preference. It is a practical protection against deals that unravel due to regulatory issues.

— HL

How Beyondhorizons supports your financing decisions

Financing decisions of any scale carry legal risk. Whether you are a business owner evaluating a direct loan facility or a corporate treasury team structuring a cross-border credit arrangement, the terms you agree to today shape your options for years.

Beyondhorizons is a Singapore-headquartered law firm with lawyers from Magic Circle and US white-shoe firms, ranked on Chambers, Legal 500, and Asia Legal Business. The team advises on corporate finance transactions across APAC, including loan structuring, due diligence, covenant review, and cross-border compliance. Clients include regional banks, US-listed companies, and Singapore government-linked entities. If you are weighing direct versus indirect lending for a significant transaction, Beyondhorizons can help you structure the deal correctly from the start.

FAQ

What is the main difference between direct and indirect lending?

Direct lending connects a borrower directly with the capital source, with no intermediary. Indirect lending uses a broker or dealer to facilitate the loan, which adds fees and a communication layer between borrower and lender.

Is direct lending cheaper than indirect lending?

Direct lending is typically cheaper because it eliminates broker fees, which range from 1% to 5% of the loan amount. On a $250,000 loan, a 3% broker fee adds $7,500 to the total cost.

How fast is direct lending compared to indirect lending?

Direct loans for straightforward transactions close in 1–3 business days. Indirect lending can produce initial approvals in minutes to hours, but the total process including negotiation often takes longer.

When should a business in APAC use indirect lending?

Indirect lending makes sense when a borrower’s credit profile is complex, non-standard, or unlikely to meet a single lender’s criteria. Brokers with relationships across 20–60 lenders can access capital that a direct approach would not reach.

Do I need a lawyer for a direct lending transaction?

Legal review is advisable for any loan above $500,000 or any cross-border financing structure. A lawyer can review covenants, identify unfavorable terms, and protect your interests if the loan needs restructuring later.